An analyst at a mid-sized Singapore equity fund walks into the office at 7:30am. There are fourteen sellside reports waiting. Two earnings call transcripts from overnight. A Reuters alert on a portfolio holding. A macro note from the house economist.

By 9am, he has read - really read - maybe four of them.

The other ten will be skimmed. Some will be missed entirely.

This is not a talent problem. It is a bandwidth problem. And for the first time in the history of asset management, there is a structural solution available that does not involve hiring more analysts.

The asset management industry in Southeast Asia is at an inflection point. The signals are visible to anyone paying attention: Singapore’s MAS is actively funding fintech and AI adoption through initiatives like the Financial Sector Technology and Innovation scheme. Regional sovereign wealth funds are not just allocating to AI; they are deploying it internally. Global firms opening regional offices are arriving with AI toolchains already built.

The question for mid-sized regional asset managers is not whether AI will reshape the investment process. It already is. The question is whether your firm will lead that shift or spend the next three years catching up to firms that did.

This newsletter exists to make that question easier to answer.

What “AI in Asset Management” Actually Means

There is a version of this conversation that happens at a lot of firms. Usually held in a strategy meeting, or triggered by someone reading a consultant’s report.

AI gets discussed as a future initiative. Something to pilot or perhaps form a committee around.

That version of the conversation is already obsolete.

The firms building an edge right now are not piloting AI as an add-on to their existing process. They are rebuilding the investment workflow itself around a set of complementary tools - what I call the AI ensemble.

Not one model. Not one vendor. A coordinated stack, each component doing what it does best, integrated into the moments that matter most in the investment cycle.

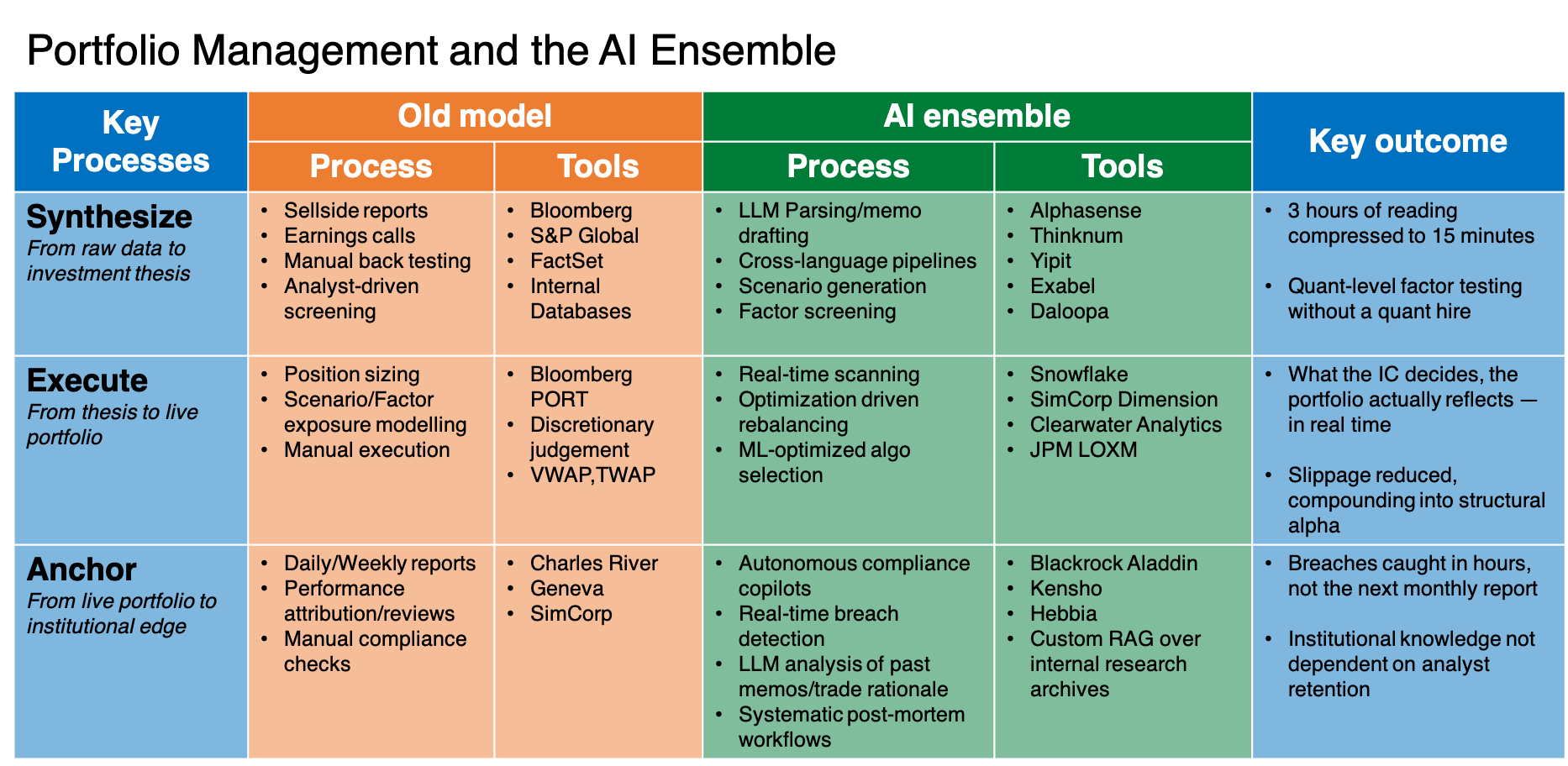

The chart below shows what that looks like across the three core processes that every asset management firm runs, every day.

The framework breaks the investment workflow into three distinct processes.

Synthesize: From Raw Data to Investment Thesis

This is where most of an analyst’s day goes. Reading. Parsing. Cross-referencing. Forming a view.

The traditional toolkit is well-known: Bloomberg for data pulls, S&P Global and FactSet for structured financial information, internal databases for historical positioning. The output is an analyst who has read enough to have an opinion, and a process that scales exactly as well as the number of analysts on the desk. Which, for many mid-sized asset managers, isn’t much.

The AI ensemble changes the input-to-insight ratio fundamentally. Tools like Alphasense and Daloopa are not search engines bolted onto research libraries. Alphasense uses language models trained on financial text to surface thematic connections across earnings calls, broker notes, and regulatory filings - connections that would otherwise require hours of manual reading to identify.

Daloopa automates the most tedious part of fundamental analysis: the extraction and normalisation of financial data from unstructured documents. What used to take a junior analyst an afternoon now takes minutes, with lower error rates.

Exabel and Yipit extend this into alternative data - the signals that do not appear in company filings at all. Consumer transaction data, foot traffic, web scraping, supply chain proxies. These were once the exclusive domain of large quant shops with proprietary data budgets. The commoditisation of access changes that calculus for mid-sized active managers.

For Southeast Asia specifically, there is a capability that does not often appear in Western discussions of AI in finance: cross-language pipelines.

A Singapore-listed consumer staples company with significant Indonesia operations will generate material information in Bahasa Indonesia. Management interviews, local press and regulatory commentary, all of which are rarely seen by most analysts at English-language firms. LLMs with multilingual capability change that. The competitive edge available to a regional firm that can actually read Southeast Asian markets - in the languages those markets operate in - is significant and underappreciated.

The outcome is not that AI replaces the analyst’s judgment. It is that the analyst’s judgment gets applied to a dramatically richer information set. Three hours of reading compressed to fifteen minutes. Quant-style factor screening available without a dedicated quant hire.

Execute: From Thesis to Live Portfolio

This is where the gap between intention and outcome has historically lived.

The Investment Committee meets. A view is formed. The portfolio manager knows what the target allocation should look like. What happens between that decision and the actual portfolio - the sequencing of trades, the timing within each session, the management of market impact - is where slippage accumulates.

The traditional execution model relies on portfolio management systems like Bloomberg PORT, discretionary trader judgment on timing, and standard algorithms (VWAP, TWAP). They do not adapt to intraday liquidity conditions. They do not dynamically rebalance around transaction cost estimates. And they do not optimise across the interaction effects of multiple concurrent positions.

The AI execution layer changes all three of these.

SimCorp Dimension and Clearwater Analytics provide the portfolio-level infrastructure: real-time position reconciliation, exposure modelling, constraint monitoring. But it is the algo execution layer that represents the sharpest change. JPMorgan’s LOXM is the best-known institutional example of ML-optimised execution: a model trained on millions of historical trades that selects and parameterises execution strategies dynamically, based on real-time market microstructure.

The result is measurable reduction in implementation shortfall. Not marginal, but structural over time.

For most mid-sized regional asset managers, the direct access to a system like LOXM is constrained by prime brokerage relationships. But the principle applies across accessible alternatives, and the direction of travel for algorithmic execution is unambiguous: static VWAP as the default execution strategy will look increasingly primitive within five years.

The more immediate opportunity is at the Snowflake layer - using cloud data infrastructure to close the loop between IC decision-making and portfolio reality in real time. The problem many mid-sized asset managers have is not that they make bad decisions; it is that the portfolio does not fully reflect their decisions because the execution and reconciliation cycle is too slow. Real-time data infrastructure, paired with optimisation-driven rebalancing tools, closes that gap.

What the IC decides, the portfolio actually reflects in real time. That is the outcome that matters.

Anchor: From Live Portfolio to Institutional Edge

This is the process that most AI discussions in asset management underweight, and where I believe some of the most durable competitive advantages will be built.

Anchoring covers everything that happens after the trade. Compliance monitoring, performance attribution, portfolio review, and the institutional memory that turns individual decisions into organisational knowledge. In the traditional model, this is largely backward-looking and manual: daily and weekly reports, periodic performance reviews, manual compliance checks against investment guidelines.

The costs of this model are less visible than they should be. Compliance breaches caught in the monthly report rather than the hour they occur. Post-mortem analysis that never actually happens because the team is too busy preparing for the next IC meeting. Institutional knowledge that lives in the heads of two or three senior people - and walks out the door when they leave.

BlackRock’s Aladdin has anchored large institutional portfolios for years, providing the risk modelling and compliance infrastructure that most mid-sized regional firms cannot build themselves. But Aladdin is primarily a risk system, not a knowledge system.

The newer tools in this layer are Hebbia and Kensho, paired with custom RAG implementations over internal research archives. They represent something different: the beginning of genuine institutional memory at the AI layer. Hebbia allows firms to build retrieval systems over their own document corpus: past investment memos, trade rationale notes, IC minutes, research archives going back years.

The ability to ask a question of your firm’s own history - “what was the investment committee’s view on Indonesian consumer exposure in 2019, and what happened to the positions that reflected that view?” - is a capability that no junior analyst on the team has, and that the senior PM who was there may not accurately recall.

Real-time breach detection, autonomous compliance copilots, systematic post-mortem workflows: these are not features. They are the difference between a firm whose institutional knowledge compounds over time and one that resets every time a key person leaves.

Why This Matters for SEA Asset Managers Now

The ensemble is not a future roadmap. Every tool named in this framework is available today, to firms willing to engage with the integration work required to make them interoperate.

That integration work is real. It is the part that consultants’ slide decks tend to understate. Connecting Alphasense outputs to an internal research workflow, building a RAG layer over a proprietary document archive, configuring real-time data pipelines between execution and portfolio management systems - none of this is plug-and-play.

But the firms that do it are not building a marginal improvement. They are building a different kind of investment operation: one where analysts think at higher abstraction levels, where the portfolio actually reflects IC intent, and where institutional knowledge does not decay when people leave.

In a regional market where the talent pool for investment professionals is finite and the competition for assets under management is intensifying - from global firms with larger balance sheets and from robo-advisory platforms attacking the retail segment - operational alpha is not a nice-to-have. It is a strategic imperative.

The next issues of Buyside AI will go deep on each of the three processes: how the synthesise stack actually gets built, what the execution layer looks like in practice for a regional active equity fund, and how to think about the anchor layer as a knowledge infrastructure problem rather than a compliance problem.

If you are building this at your firm, or thinking about how to start, I want to hear from you.

Buyside AI covers AI adoption across the investment workflow, with a focus on mid-sized active managers operating in Southeast Asia. If this issue was useful, forward it to one colleague who should be reading it.